{kind=link}

Accounts payable and receivable are required to ensure your cash flow and spending are appropriately tracked. While these names sound very similar, understanding how these two types of accounts differ is essential, so you don’t accidentally mix them up.

In this guide, we explore the differences between accounts receivable and accounts payable and explain why they are so important for businesses.

QuickBooks can help you manage your accountsQuickBooks is our top pick for accounting software, with its many capabilities and features. To save you time and effort, QuickBooks can automatically pull information from your bank accounts and balance your books — so all you have to do is review the entries. |

Featured Partners: Accounting Software

What is accounts receivable?

Accounts receivable (often abbreviated as “AR”) is a general ledger account that captures short-term payments owed to your business. Accounts payable are considered a current asset since they represent outstanding payments, and they are listed alongside other assets on the chart of accounts.

An accounts receivable entry is created when your company lets a person or organization buy your goods or services on credit. Some examples of accounts receivable entries include credit card purchases, unpaid invoices and upcoming subscription or installment payments due within the next few months.

After the payment is received, the entry is credited (subtracted) from your accounts receivable and debited (added) to your cash account. You can learn more about the difference between debits vs. credits in our helpful guide. If you use accounting software such as QuickBooks, you can link your bank accounts and the system will automatically log the appropriate credits and debits in the correct accounts. This chart captures the accounts receivable workflow:

If the customer never pays the outstanding balance, it’s written off as bad debt expense or a one-time charge. Your business might also be able to resell the debt to a third party in a process known as AR factoring or accounts receivable discounted.

What is accounts payable?

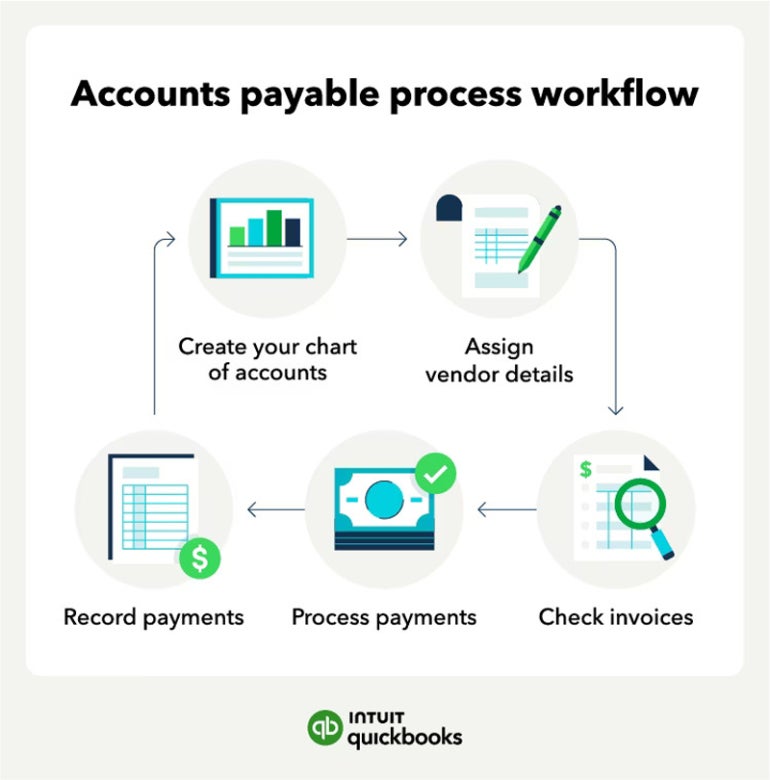

Accounts payable (often abbreviated as “AP”) is a general ledger account that captures short-term payments owed to creditors, suppliers and vendors. Accounts payable are considered a current liability since they represent outstanding payments, and they are listed alongside other liabilities on the chart of accounts.

Some examples of short-term entries that might be recorded under accounts payable include raw materials, supplies, equipment, power and electric bills, transportation and service costs. Accounts payable entries must be paid off within a certain time frame to prevent defaulting on the debt. Some common payment terms for accounts payable entries are 30, 45, 60 and 90 days.

When you receive an invoice from a vendor or supplier, you will credit the amount to your accounts payable and debit the correct expense account. Accounting software like QuickBooks makes tracking accounts payable automatic and easy, just as with accounts receivable. This chart captures the accounts payable workflow:

Longer-term payments, such as mortgages, are typically not listed under accounts payable. However, upcoming monthly payments for those mortgages (which are due in the short term) would be listed on account payable, for example. Wages owed to employees are also usually recorded separately in a different account dedicated to payroll. Properly categorizing and tracking payments is essential for optimizing accounts payable.

Key differences between accounts receivable and accounts payable

Accounts receivable are two sides of the same coin: Both of them record short-term transactions that have not been paid. The key difference is that accounts receivable captures money that is owed to your business by third parties, while accounts payable captures money that your business owes to other organizations. In other words, accounts receivable is incoming money that your business will receive in the future, while accounts payable is outgoing money that your business will pay in the future.

Accounts receivable and accounts payable importance for businesses

By comparing accounts receivable and accounts payable together, you can get a picture of the short-term financial health of your business. Delving deeper into each of these accounts will help you see how transactions are occurring across your business and unlock the strategic value of both accounts payable and receivable.

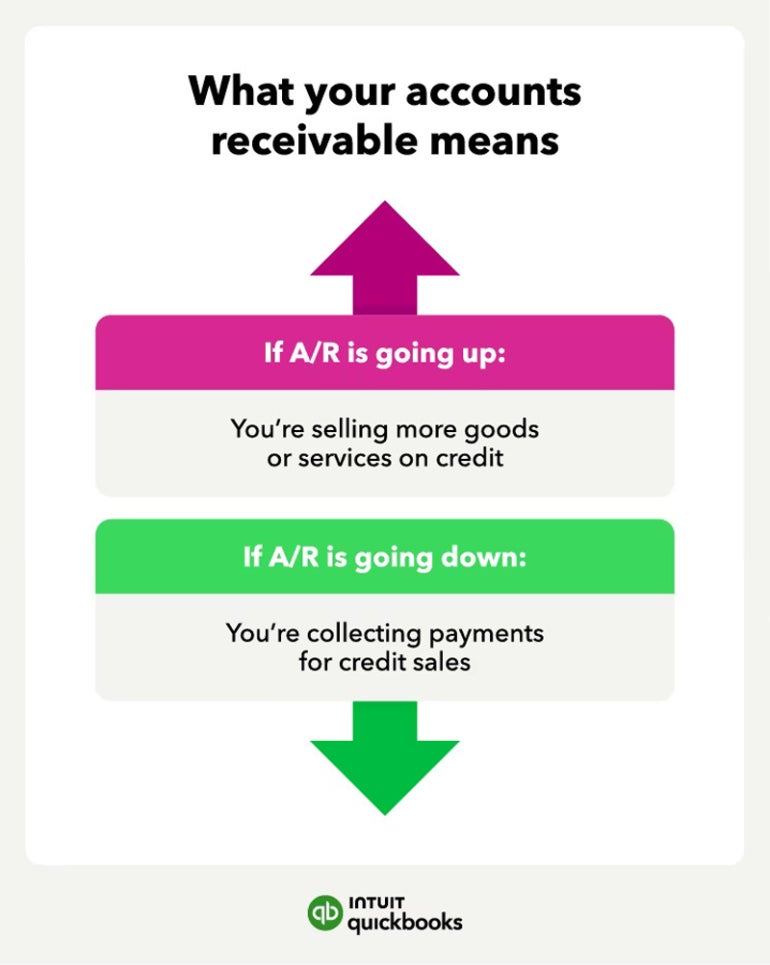

If your accounts receivable keeps going up from month to month or quarter or quarter, that might mean that you’re making more and more sales on credit or that customers aren’t paying outstanding invoices. If accounts receivable goes down, that could mean that your customers are paying off outstanding invoices quickly or that they aren’t making as many purchases on credit. Looking at the details of your accounts receivable is crucial for determining why the numbers are going up or down.

If accounts payable increases from month to month or quarter or quarter, it means a company is buying more goods and services on credit than it is paying off. If accounts payable decreases, it means that a company is paying off its short-term outstanding debts faster than it is accruing them.

Looking back over historical accounts receivable and accounts payable data will also help you determine your own payment patterns as well as the payment habits of your customers. Accounts receivable will show if your customers pay on time or early, or if they tend to run late or only make partial payments. Accounts payable will reveal whether or not your business pays its own obligations early, on time or late. This information can help you take advantage of early payment discounts and avoid unnecessary late fees.

How to handle accounts payable and receivable

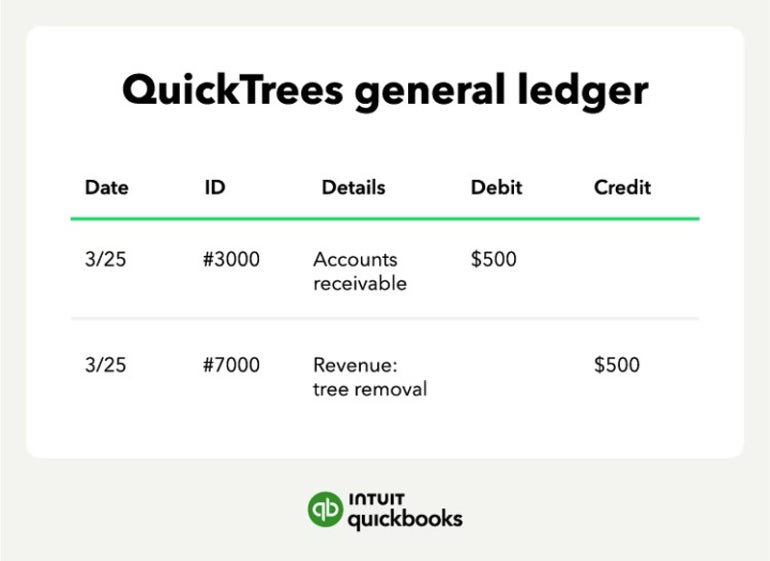

In double-entry accounting, each transaction must have two entries that even each other out: a debit (addition) and credit (deduction). After you generate an invoice for unpaid goods or services you have provided to customers, you will debit that amount to your accounts receivable and debit the appropriate sales account, as demonstrated below:

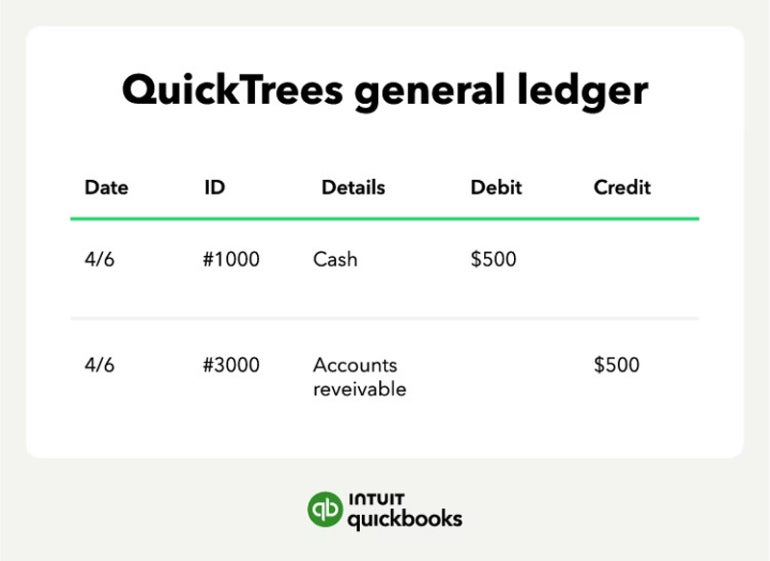

Once the customer eventually pays the invoice, you will credit your accounts receivable and debit your cash account to capture the incoming money, as shown here:

Increases in accounts payable are always recorded as a credit. After you receive an invoice for goods or services that your company has purchased on credit, you will credit that amount to your accounts payable and debit the appropriate expense account. After you pay that outstanding invoice, you will debit the accounts payable and credit your cash account to capture the outgoing money.